How Currency Conversion Fees Work and How to Minimize Them

Cross-border transactions are a daily thing in the modern economy around the world. Businesses and individuals make such transactions daily without any reservations. Currency conversion is bound to happen whether you have to purchase something online from a foreign retailer, travel abroad, or collect payments from foreign clients. However, understanding how currency conversion fees and foreign transaction fees work and ways of minimizing them saves you a lot. Our clients are the people we want to see more successful financially. So, at Eximpe, we want to give them the knowledge that can help them make better financial decisions.

What Are Currency Conversion Fees and Foreign Transaction Fees?

Whenever you transact in a currency different from your account’s base currency, your bank or payment provider must convert the funds. This process isn’t free. There are two main types of charges you’ll encounter:

- Currency Conversion Fees

These are fees that are levied on the money when it is converted from one currency to another, usually by banks, card networks or payment operators. The fee ranges from 1%–3% over the mid-market exchange rate but may go as high as 12% with Dynamic Currency Conversion (DCC) at point-of-sale terminals.

- Foreign Transaction Fees

These are additional charges (1%–3%) charged by your bank or card issuer for a transaction done in a foreign currency in addition to a potential markup from a currency conversion. They pay for International payment processing and security.

How Do These Fees Affect You?

Let’s break down a typical international transaction:

- Exchange Rate Markup: Assume you’re purchasing a product that costs $100. The mid-market exchange rate is ₹83 per dollar, so the product should cost ₹8,300. But if your bank charges an exchange rate of ₹81 per dollar (as a result of a 2.5% markup), you’ll end up paying ₹8,500.

- Foreign Transaction Fee: In addition to this, your bank may also levy a 2% foreign transaction fee, taking an additional ₹170 off your bill.

- Dynamic Currency Conversion (DCC): If you choose to pay in your local currency at checkout (available with some retailers), you might incur an additional 2.6% to 12% markup-making the transaction even costlier.

These fees may seem small, but they add up quickly, especially for frequent international transactions or large business payments.

Common Triggers for Fees

| Fee Type | Typical Range | Triggered By |

| Currency Conversion Fee | 1%–3% (up to 12%) | Currency exchange, DCC at POS, online payment platforms |

| Foreign Transaction Fee | 1%–3% | Purchases abroad, foreign websites, ATM withdrawals |

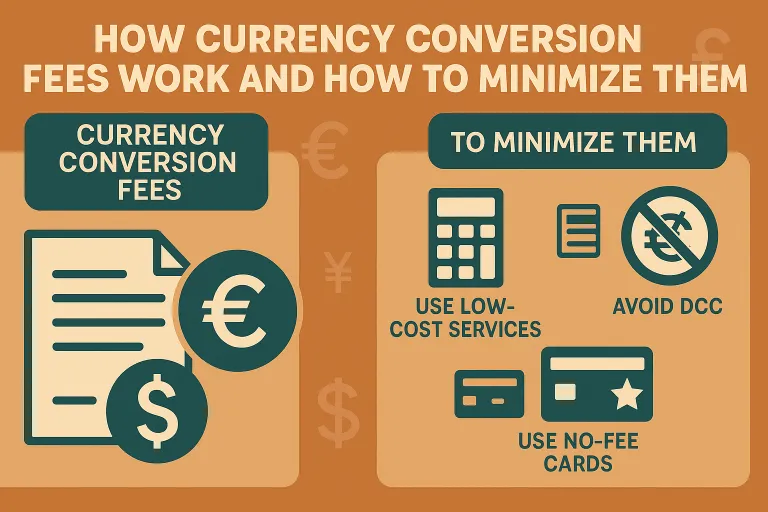

How to Minimize Currency Conversion and Foreign Transaction Fees

Choose the Right Payment Method

- Use specialized payment platforms or fintech solutions (i.e., Eximpe) offering competitive exchange rates and transparent fee schemes. These platforms tend to offer under 1% for large currencies, as compared to the 4-6% premiums of conventional banks.

- You should consider having a multi-currency account to control as many international transactions as possible and avoid such conversion charges all the time.

Avoid Dynamic Currency Conversion (DCC)

- Always choose to pay in the local currency if offered an option at a foreign ATM or merchant. DCC will likely include embedded markups of up to 12% over market rates.

Use Cards with No Foreign Transaction Fees

- Certain credit cards are especially for foreign use and don’t levy foreign transaction fees. Look up and apply for these types of cards and save on each foreign purchase.

Leverage Fintech and Online Currency Exchange Platforms

- Such platforms as Eximpe and other top fintech suppliers provide live exchange rates, reduced markups, and quicker processing speeds than traditional banks.

- These sites also offer transparency, so you can see precisely how much you’re paying in currency conversion charges.

Time Your Transactions Wisely

- Currency exchange rates can fluctuate. Scheduling transfers during mid-month or on weekdays can sometimes result in lower fees and better rates, as banks are less busy and rates are more stable.

Plan for Larger Withdrawals

- If you need cash abroad, withdraw larger amounts at once to minimize the number of transactions and associated ATM and conversion fees.

Why Eximpe?

Here at Eximpe, we are dedicated to delivering our customers with the best possible rates and upfront fee arrangements for every currency conversion service you may need. Through our platform, you can:

- Gather payments from more than 130 nations

- Access USD, GBP, CAD, EUR, and other local accounts

- Enjoy true real-time exchange rates and low markups

- Prevent surprise charges and optimize your global revenue

Final Thoughts

Foreign transaction fees and currency conversion are part of international business. Still, you can limit their influence if you understand how it works and know who to make partners with, such as EximPe. Even little cuts on a single transaction can make huge differences in the long-range plan. Stay informed, plan, and leave your cross-border payment under the management of EximPe since every saved rupee will increase your profits.

FAQs

1. What is the difference between currency conversion fees and foreign transaction fees?

Currency conversion fees are charged for converting one currency to another, often as a markup on the exchange rate. In contrast, foreign transaction fees are extra charges (usually 1–3%) applied by your card issuer or bank for processing payments in a foreign currency or through a foreign bank.

2. How can I minimize these fees when making international payments with Eximpe?

Use Eximpe’s platform for competitive exchange rates and transparent, low fees (often under 1% for major currencies), avoid Dynamic Currency Conversion (DCC) at checkout, and consider multi-currency accounts to reduce unnecessary conversions.

3. Why should I avoid Dynamic Currency Conversion (DCC) when paying abroad?

DCC lets you pay in your home currency at foreign merchants but usually comes with much higher markups (up to 12%), making your transaction more expensive than paying in the local currency.